We understand that there are important decisions that need to be made around how and when you retire.

If you are thinking about retiring, our video and the information below tell you more about the process.

It's good to think ahead, as you will have some decisions to make. You will need to decide on the date you want to retire and what benefits you want to take.

To help you, you can find out about the pension benefits you have built up so far by logging into your My Pension account. You can use the calculator in your My Pension account to work out what you will get on your planned retirement date. And you can also speak to your employer, who can give you more information about what steps you need to take. Elected members (councilors and mayors) do not have access to the calculator in My Pension, as different rules may apply, so please speak to your employer.

GMPF also holds pre-retirement events to help. Visit our Events section to check if we are visiting a region close to you or holding an online event.

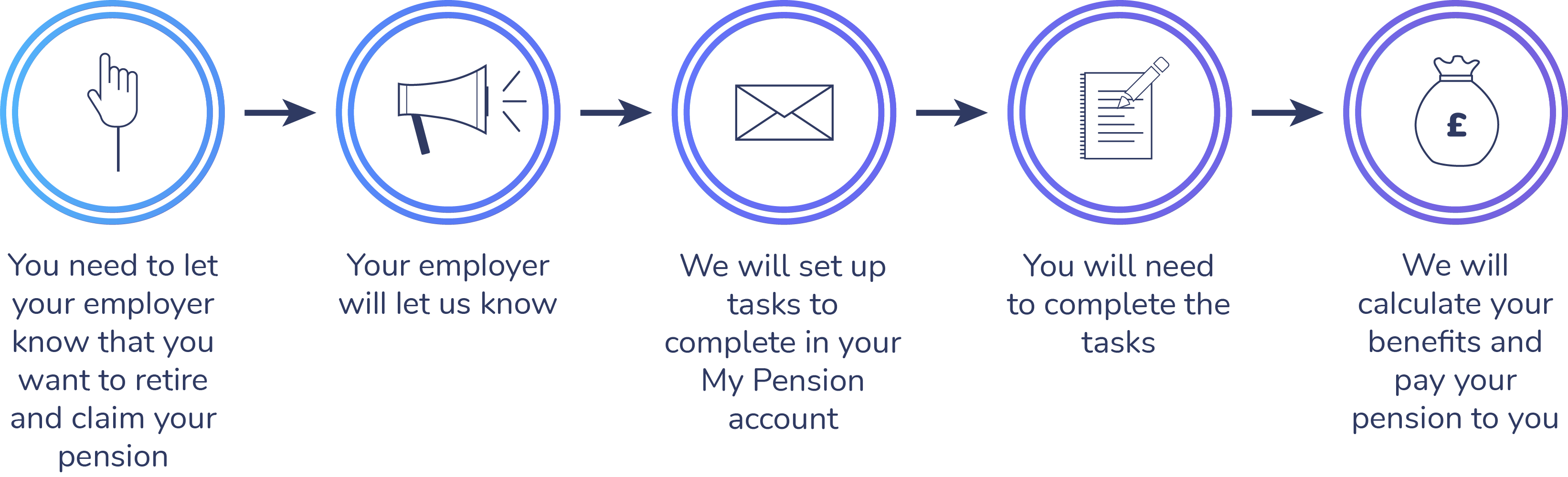

The retirement process has a number of stages:

1. How do I notify GMPF of my retirement?

You don’t need to. If you are intending to retire and want to claim your pension, simply notify your employer. Please check directly with your employer to find out how much notice they require. They will then send us the notification and information we need.

2. What information does my employer provide?

Your employer will provide us with your pay figures up to your last day of work, as we don’t have direct access to your pay information. Unfortunately, we are unable to get this information directly from you.

3. What happens when GMPF receives the pay information?

We check the information for accuracy. If we find any inconsistencies, we query them with your employer and in some cases request further information. This can cause a slight delay while we resolve the query.

Once we are happy with the information we will create tasks for you to complete through your online My Pension account. We will email you to you to inform you when the tasks are available. If you have elected for paper communications we will send you a paper copy of your retirement documents.

4. What do I need to do when I receive my retirement tasks or documents?

Your retirement tasks or documents will contain full details of how your pension has been calculated with two quotes:

- One quote will show the maximum pension you could receive.

- The other shows the maximum lump sum you can take.

If you have any Additional voluntary contributions (AVCs) or Additional pension contributions (APCs) they will be included in the figures unless otherwise stated.

We aim to process the information and produce your retirement information within 15 working days of receiving the information we need from your employer. If there are any expected delays, if we have your email address, we'll email you to let you know.

Once you receive your retirement information you will need to complete the member’s retirement form (P71m) by completing your tasks. We will need to see evidence of your date of birth. This can be a valid passport, valid photo card driving licence or birth certificate.

If you have elected for paper communications we will send you a paper copy of your retirement documents.

5. What happens when GMPF receive my completed tasks or forms?

We check that we have all the information we need. If any of the information is missing or unclear, we will set up additional tasks to complete. Any incomplete paper forms will be returned to you.

We use the pension information you have provided to check against the lump sum allowance to ensure you haven’t gone over the limit. We also check your pension against the annual allowance.

If we have your email address, we'll email you throughout the process to keep you up to date.

Finally your pension is put into payment according to the election you have made.

We aim to pay any lump sum as soon as possible following your retirement date. However, if you have an AVC that you have been contributing to up to your last working day, it may delay payment of your pension as we have to wait for all the payments to be passed from your employer to our AVC provider, and for them to disinvest your money.

6. Things to consider

- Your pension payment will be the last working day each month. It is treated as income and is therefore taxable.

- We cannot pay any part of your pension before your retirement date even if we have all the information we need.

- If you exceed your lump sum allowance and/or annual allowance there may be tax implications that need to be dealt with before we can put your pension into payment.

- We return any original documents using the same method we received them, for example if we receive it via recorded delivery we will return it the same way.

- We do not return photocopied documents unless specifically requested.

7. Additional voluntary contributions (AVCs)

If you have paid additional voluntary contributions (AVCs) to build up a separate pot of money for your retirement, we cannot pay your main scheme benefits until your AVC choice is also ready to be paid.

Disinvesting your AVCs takes time, and your AVC provider will not start disinvesting until your retirement date. It is therefore important that you plan for a possible delay in paying your pension. Read on for further information on the timescales for disinvesting AVCs and how to reduce possible delays.

Additional information about accessing your AVCs, including how to book an appointment with an advisor from Pension Wise, is available on our 'Ways you can top up your pension' webpage.

Tax free cash from AVC fund

If you decide to take a tax free lump sum from your AVC fund, we'll ask your AVC provider to pay it to us, so it can be paid with your main scheme benefits. It can take up to one month for your AVC provider to disinvest and pay it to us from when you tell us your decision, or up to one month from your retirement date, if this is later.

Your AVC provider will not begin disinvestment until you have reached your retirement date. This is usually because of the way AVCs are collected. Your employer may still need to pay your final contributions to them, which can sometimes happen in the month after you have retired. To reduce additional delays from waiting for your final payment to be sent over by your employer, you can choose to end payment of your AVCs a couple of months before your retirement date.

Even if you have stopped paying your AVC contributions before you retire, your AVC provider will not begin disinvestment until you have reached your retirement date.

Please be aware that your AVCs are taken from your pay before income tax is deducted. If you stop paying your AVCs before your retirement date, you’ll lose the tax relief on those contributions.

If you pay into your AVC fund using a salary sacrifice option your employer may offer, you’ll be paying less income tax and national insurance contributions, often making your take home pay higher. If you stop paying your AVCs before your retirement date, you’ll lose this benefit.

Annuity procedure

If you decide to use your AVC fund to buy extra pension (also known as an annuity), we will obtain quotes from your AVC provider. It can take approximately two weeks for your AVC provider to send us the quotes from when you tell us your decision, or approximately two weeks from your retirement date, if this is later.

Your AVC provider will not provide their quotes until you have reached your retirement date.

We'll then send the quotes to you to compare to the Scheme annuity quote you'll have received with your retirement pack. You also have the option to obtain quotes direct from other annuity providers.

If you opt for a Scheme annuity, we must then wait for your AVC to be disinvested, which can take up to one month. Once we have received the final AVC fund value, we'll calculate the amount of extra pension it has bought and pay this with your main scheme benefits.

If you opt for an annuity from your AVC provider or another provider you choose, they'll arrange payment direct with you. We'll proceed with payment of your main scheme benefits at the same time.